As early as Thursday, January 16th, before the market opens in Europe, the Taiwanese semiconductor manufacturing giant, Taiwan Semiconductor Manufacturing (TSMC), will publish its financial results for the fourth quarter of 2024. Analysts expect the largest profit growth since 2022, driven by strong demand for artificial intelligence-related systems. Recent sales data for December suggests a further acceleration of this trend in 2025.

Key expectations:

Start investing today or test a free demo

Open account Try demo Download mobile app Download mobile app- Earnings per share (EPS): Expected $2.20-2.22 (forecasts indicate a 51% year-over-year increase)

- Revenue: $25.92 billion (TSMC's forecast is $26.1-26.9 billion, actual data based on monthly sales data indicates $26.3 billion).

- Net income growth: Approximately 55% year-over-year (average growth seen by Wall Street analysts)

Expectations in Taiwanese currency:

- Revenue for Q4 2024: NT$868.5 billion ($26.3 billion), which meets TSMC's forecasts (NT$835-861 billion) and represents an increase of approximately 39% year-over-year

- Revenue for 2024: NT$2.894 trillion ($87.4 billion), a 33.9% year-over-year increase – the highest result since the company's stock market debut

- Estimated net income for Q4 (Bloomberg consensus): NT$369.84 billion

- Estimated gross margin: 58.5%

- Estimated operating margin: 48.1%

Expectations regarding future guidance:

- Estimated sales for Q1: $24.43 billion

- Estimated gross margin for Q1: 56.9%

- Estimated operating margin for Q1: 46.4%

- Estimated capital expenditures for the year: $35.14 billion

- Expected EPS in 2025: $9.05, which implies a 29% year-over-year increase

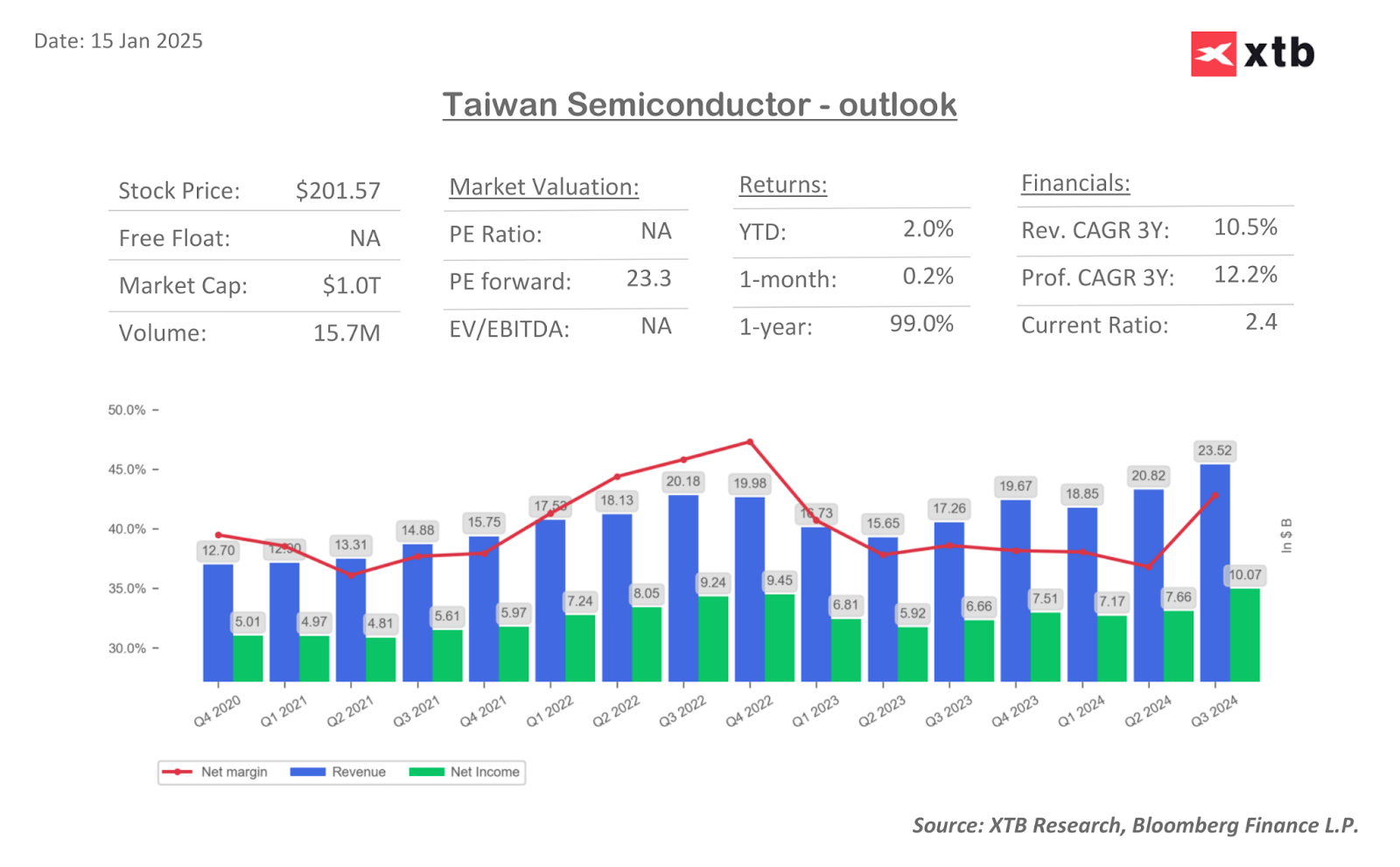

In Q3, the company presented record-breaking results in terms of revenue and profits, significantly improving margins. At the same time, the company still presents relatively low valuations from a ratio perspective. Source: Bloomberg Finance LP, XTB

What speaks in favor of publishing a strong report?

- Strong and accelerating demand for artificial intelligence-related systems: December sales data, showing a 58% year-on-year increase, indicates further dynamic growth in this segment and confirms that TSMC is the main beneficiary of this trend. The High-Performance Computing (HPC) segment remains a strong growth driver for TSMC.

- Meeting Q4 sales forecasts: Published data confirms that TSMC achieved its planned targets.

- Positive trends in profits: TSMC regularly exceeds analysts' profit expectations.

- Relatively low valuation compared to the competition: The P/E ratio (forecasted for 2025) for TSMC is 23x, which is lower than for Nvidia (31x) and ASML (30x), and comparable to AMD (23x). This, combined with growth prospects, makes TSMC a fairly attractive company.

Potential challenges:

- Short-term headwinds in the semiconductor industry: Needham analysts point to a slowdown in the automotive and industrial sectors, pressure on memory prices, and weak consumer demand.

- Margin pressure from older technologies: Bloomberg Intelligence points to potential pressure on margins from weaker demand for older semiconductors.

- Trump's presidency: Trump may want to impose trade tariffs on Taiwan as well. In addition, relations with China may worsen. Therefore, the low ratio valuation, although attractive, may also contain risks related to geopolitics.

Key issues to observe during the earnings conference:

- Prospects for building production capacity and revenue from advanced CoWoS packaging: These will provide insight into the expected demand for AI chips over the next 12-18 months.

- Progress in starting up the Arizona factory: Key to meeting the chip production needs of Apple, Nvidia, and other companies in the US. This will largely be able to mitigate the risks associated with tensions with China and potential new tariffs.

- Capital expenditure plans for 2025: These will signal TSMC's confidence in demand for next-generation N2 technology.

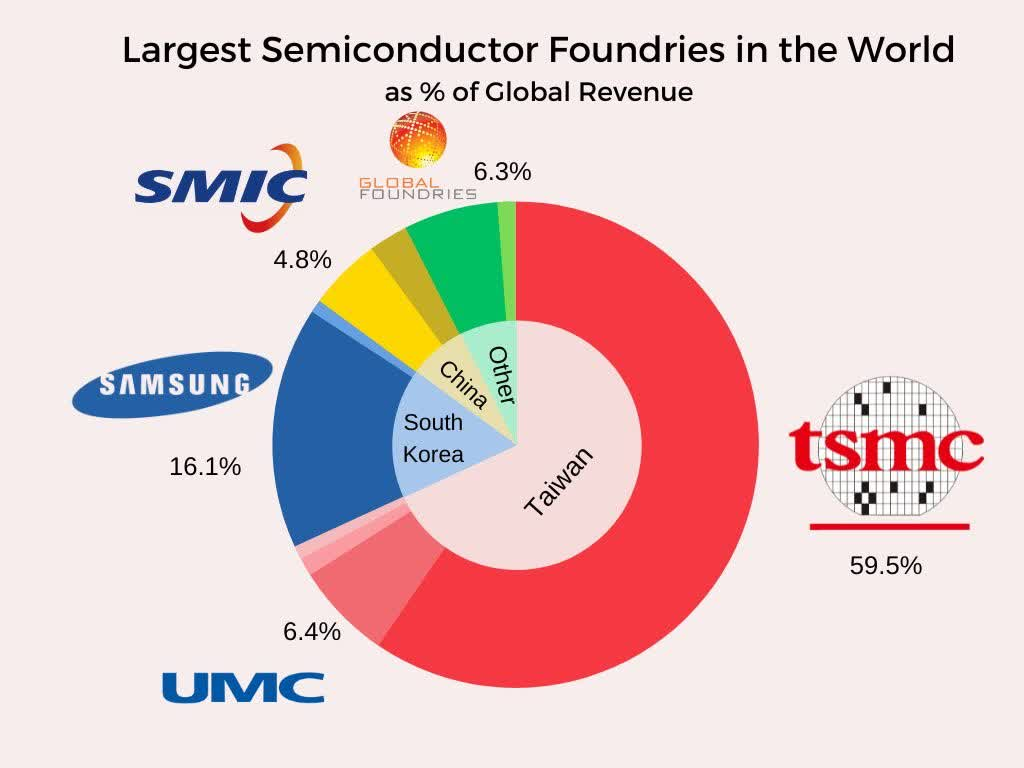

TSMC is the largest player in the semiconductor market in the world. Source: TSMC

TSMC will most likely enter 2025 with strong momentum, and considering the further development of artificial intelligence, the company's products will enjoy increasing demand. The company accounts for over 60% of the semiconductor market in the world and presents the most advanced products, which are supplied to companies such as Nvidia and Apple. At the same time, however, there are risks associated with China and trade tariffs, although by building a factory in the US, some of this risk may be neutralized, so information on this will be under investor scrutiny.

Since the publication of the results for Q4 2023, TSMC's shares have increased by over 80%. However, looking closely at one year of return (i.e., before the publication of the aforementioned results), shares are up over 100%. This means that the surprise for last year's results was very strong, which is also expected of TSMC now. During the same time, Nvidia's shares increased by 137%. TSMC shares are gaining 1.7% today in NYSE trading. If the company meets or exceeds expectations, a similar price jump as last year is possible, which would open the shares to new highs above $220 per share. On the other hand, implied volatility also suggests that in case of disappointment, shares could fall below $190 per share, which would mean the lowest levels since the beginning of December 2024. Source: xStation5

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.