- European indices closed today’s session higher. The FTSE and CAC40 posted slight gains, while Germany’s DAX rose by over 0.5%. In the US, stock indices are limiting the sell-off triggered by higher-than-expected January CPI data. However, the Dow Jones is still down 0.4%, the S&P 500 is losing nearly 0.2%, while the Nasdaq 100 is trading flat.

Today’s US inflation data came as a strong surprise to the markets, raising concerns about a further delay in potential Fed rate cuts:

- US CPI for January (YoY): 3.0% (Forecast: 2.9%, Previous: 2.9%)

- US monthly CPI (MoM): 0.5% (Forecast: 0.3%, Previous: 0.4%)

- Core CPI YoY: 3.3% (Forecast: 3.1%, Previous: 3.2%)

- Core CPI MoM: 0.4% (Forecast: 0.3%, Previous: 0.2%)

- Initial gains were reversed by the US dollar index, which is now trading flat after investors priced in a lower likelihood of a trade war following comments from White House officials. A statement from the Irish Department of Foreign Affairs, which provided positive updates from talks between senior EU and US officials, supported EUR/USD. After an initial 0.5% drop, the pair rebounded by nearly 0.4% to around 1.04.

- Following the US data, the market now expects Fed rate cuts only by late 2025, in contrast to earlier forecasts, which had fully priced in a cut by September 2025. The yield on 10-year US Treasury bonds rose by over 9 basis points to 4.63%, while 2-year yields increased by 7 basis points to 4.36%.

- Shares of major US defense companies such as Lockheed Martin and General Dynamics are declining today, extending recent sell-offs. Investors are pricing in higher chances of a peace agreement in Ukraine after Donald Trump held phone conversations with Zelensky and Putin, indicating that negotiations may take place soon.

- SMCI is gaining around 5% following optimistic forecasts for 2026, along with assurances that pending financial reports will be published on time. The Nasdaq exchange extended the company’s reporting deadline to February 25.

- Brent crude oil (OIL) is down more than 2% after US weekly crude inventory data exceeded expectations. According to the EIA report, stockpiles increased by 4.07 million barrels (compared to a forecast of 3 million barrels). Natural gas contracts saw slight gains today, rising by 1.5%.

- In the precious metals market, prices rebounded in the second half of the session after volatile moves triggered by inflation data. Gold was down more than 1% at its lowest point but has now returned above $2,900. Silver is up over 1.3%, while platinum has gained 0.7%. Palladium is the weakest performer, down about 0.5%.

- Among agricultural commodities, ICE cotton futures recorded the strongest gains, while CBOT soybean futures suffered the largest losses, declining nearly 2%.

- Sentiment in the cryptocurrency market has improved slightly after the dollar weakened. Bitcoin reversed its earlier decline and is now back at $97,000. Polkadot and Binance Coin lead gains among major cryptocurrencies, rising 8% and 6%, respectively.

Start investing today or test a free demo

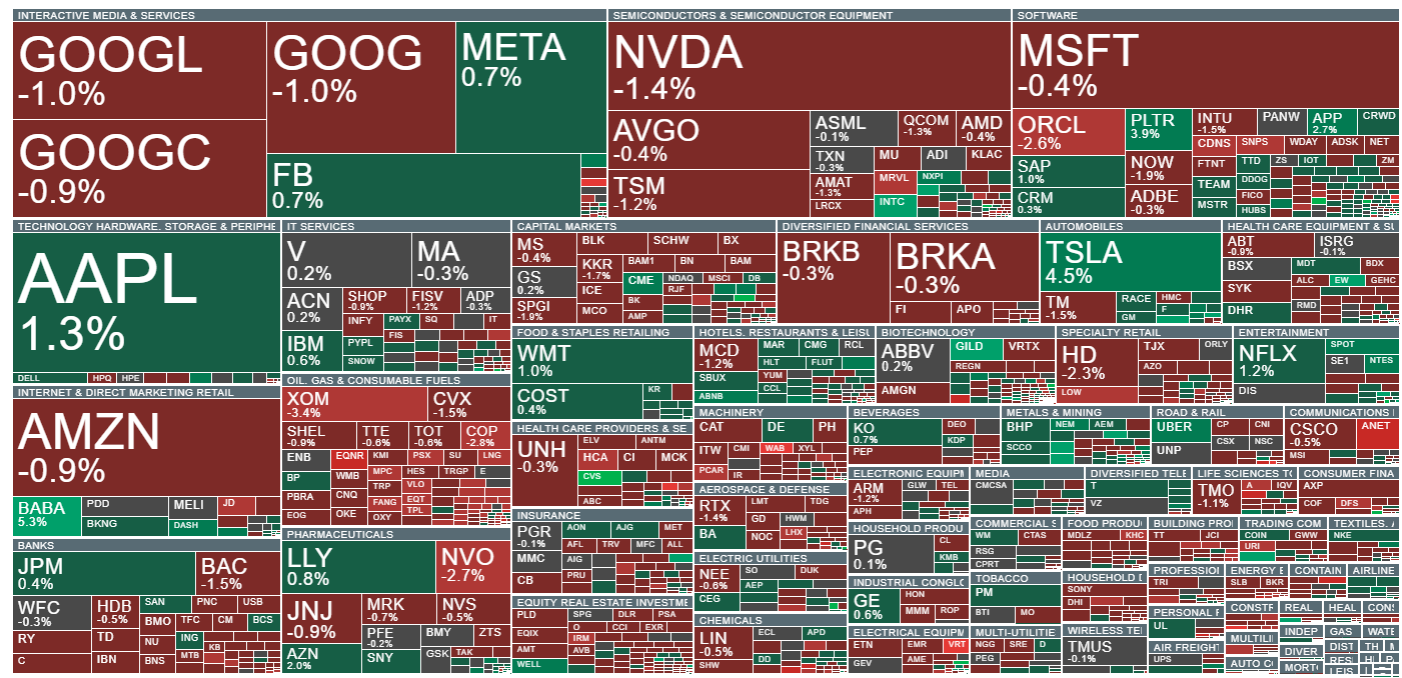

Open account Try demo Download mobile app Download mobile appTechnology stocks are seeing strong gains, led by Tesla and Alibaba ADRs. In the semiconductor sector, Intel is outperforming, while in software, Palantir, Salesforce, and Applovin are among the top gainers.